Investment Thesis of MTY FOOD GROUP (MTY)

07/12/2021

1. SUMMARY

MTY FOOD GROUP. Ticker (MTY) current share price 57 Canadian dollars

-

Fast food franchise company.

-

Recurring revenues due to its royalty-based business model.

-

Revenue CAGR 23% over the last 10 years.

-

Resilient model to financial crises.

-

Excellent track record in making acquisitions.

-

Aligned management team.

-

Fragmented market with growth potential.

1.1. History

MTY Food, founded in 1979 by Stanley Ma, is one of Canada's largest restaurant franchises and is becoming a major player in the United States through a strategy of mergers and acquisitions with an excellent track record, financed mainly by debt and FCF, and currently has 80 different brands including fast food, ice cream and similar brands.

It is worth noting that MTY receives 90% of its revenues through royalties, as the company does not operate the restaurants, which makes its business model more attractive and with lower operating risk.

The following image summarises the most important milestones of the company:

2. BUSINESS ANALYSIS

This section will explain in detail MTY's business profile, its sources of revenue generation and the M&A strategy that the company has followed in recent years.

2.1. Business profile

MTY's business consists of franchising and operating corporate-owned locations of quick service and casual dining restaurants, as well as the sale of retail products. The company also operates a food processing plant, and a distribution centre.

The company has numerous restaurant concepts, allowing it to position itself in a wide range of demographic, geographic and economic sectors.

The following image shows MTY's various brands, which protect the company from changes in consumer preferences:

The brands that have the largest weight in system sales (sales of all existing restaurants, including those that have closed or opened during the current financial year, as well as sales of new concepts acquired from the closing date of the transaction and onwards) are: Papa Murphy's and Cold Stone Creamery. These two brands currently account for over 45% of system sales, generating approximately 31% and 18% of sales respectively.

Taco Time, Thai Express and Baja Fresh Mexican Grill are the third, fourth and fifth largest concepts in terms of system sales, each generating less than 10% of network sales.

On the other hand, it is important to mention that the company has some seasonality in sales, this is due to the fact that sales of frozen treats and shakes are higher in Q2 and Q3, in addition, pizza sales have a higher demand on Halloween, the following image clearly shows this seasonality.

With regard to the type of locations of the MTY group, these can be classified into:

-

Food courts, office towers and shopping centres.

-

Street front.

-

Non-traditional format within airports, hospitals, campuses, convenience stores, supermarkets, cinemas, amusement parks and other retail locations or shared sites.

It should be noted that MTY has made a shift in its business model in recent years, where there has been an inclination towards a particular type of restaurant location and, therefore, in the percentage they represent in the system's sales.

The following table shows this evolution:

There is a tendency towards street-front shops, which is the most attractive of the three possible options, as demonstrated by the percentages of sales they are able to generate. Their weight in sales is higher than the percentage of shops, which means that they are more profitable for the franchise (remembering that their royalties depend proportionally on gross sales).

Then, another important factor to take into account in MTY is the percentage of net closures in the year (excluding restaurants acquired by M&A operations), which has gone from being around 0% in 2010 to approximately 5.6% in 2020, although the pandemic played a fundamental role in the latter year.

The following table shows the net closure of premises in 2018 and 2019:

If we take into account the transition of the company's business model mentioned above, which is based on the reduction of the weight of restaurants in shopping centres (a model in decline in sales), it is consistent that in recent years there have been closures in the less profitable premises and it is to be expected that when the premises in shopping centres have less weight, the net closure of shops will decrease.

2.2. Sources of revenue generation:

The operation of franchises

The franchise agreements that MTY usually enters into with franchisees may vary according to the type of shop location, being longer for those with traditional locations (between 10 and 15 years) or shorter for those without traditional locations (between 3 and 5 years).

When an individual acquires a franchise from the group, they initially declare an income that can range between USD 25,000 and USD 50,000 for traditional locations and between USD 5,000 and USD 17,500 for non-traditional locations. In addition, and in accordance with the franchise agreement, the company will charge an ongoing royalty to each franchisee of approximately 3% to 7% of gross sales.

The franchisee's obligation to report gross sales generated is contractually stipulated, and may even be estimated by the point-of-sale ('POS') system installed in the shops. In the case of other items, royalties are integrated into the price of the products and are collected by the company through the distributors.

However, the Company's sources of revenue are not limited to those I have already discussed. In addition, MTY negotiates better prices with suppliers and shares a percentage of the margin it obtains with the franchisee, while the other part is an income from such negotiation.

Finally, as a noteworthy aspect, the franchise agreement may also include employee training, technical assistance and other services that the company will provide to the franchisees for a slightly higher cost, which is usually attractive as it allows to "secure" the guidelines of the parent company.

In summary, the company's revenue comes from the following sources:

1. Franchise revenues

During 2019 and 2020, revenues from this category account for 50% and 52% of consolidated revenues respectively, representing more than 90% of the Company's EBITDA.

Franchise revenues are structured internally into several line items, all of which are derived from franchise operations, as described below:

1.1. Royalties: As recently mentioned, MTY charges an ongoing royalty to each franchisee. This fee typically ranges between 3 % and 7 % of gross sales, depending on the concepts, and is usually paid on a weekly or monthly basis.

1.2. Initial franchise fee: This income is a one-off payment and is not recurring as in the case of royalties. However, MTY charges an initial franchise fee that typically ranges from USD 25,000 to USD 50,000 (USD 5,000 to USD 17,500 for non-traditional locations) at the beginning of the term of the franchise agreement.

Initial franchise fees are recognised on a straight-line basis over the term of the franchise agreement as the performance obligation associated with the franchise rights is fulfilled. Amortisation begins once the restaurant is opened.

1.3. Master licence fees: This type of income usually arises when there is an individual or entity interested in acquiring the territorial rights to a space in which the group is not yet located in order to expand the brand. MTY charges a master licence fee at the time it grants these rights.

1.4. Renewal fees: At the time the contract agreed between franchisee and franchisee expires, the franchisee has the possibility to renew the terms or extend its status as a franchisee of MTY. In this case, the company charges a fee for the renewal of the expired franchise. Depending on the concept, the fee varies between USD 1,000 and USD 5,000 per renewed year.

1.5. Revenue from the sale of franchised premises: In some cases, MTY manages the construction of a new restaurant, which is delivered 'turnkey' to the franchisee upon completion.

Revenue from the construction and renovation of restaurants is recognised upon completion of the construction and renovation work.

1.6. Sales of goods and equipment: Indirectly, another source of income for the group is that franchisees are required to purchase certain goods and equipment, which will be used at their company locations. These items, which MTY provides to franchisees, are sold at a profit.

Revenue is recognised when the goods are delivered. MTY also generates some management fees from the resale of services to its franchisees.

1.7. Rental income: In certain cases, the company may earn rental income on certain properties, leases it owns and firm rental income. This is because, as a large company, it is able to negotiate better terms on long-term leases than if the franchisee were to do so directly. A portion of the improved terms it obtains is collected by MTY.

In other words, MTY can lease the premises in which the franchisee will carry out the activity and subsequently sublease them for a fee.

1.8. Gift card revenue: MTY recognises breakage revenue on a pro rata recognition basis, which is based on the historical redemption pattern of gift cards. Such a non-redeem rate can be in the region of 10-15% of these gift cards.

1.9. Supplier considerations: MTY receives supplier considerations. Supplier contributions are recognised in the month in which they are earned.

1.10. Transfer and other fees: MTY charges a fee for the transfer of a franchise, documenting changes to the franchise agreement and other documents, providing plans and specifications for shop design and for construction supervision.

1.11. Accounting fees: For some of the group's brands, MTY is able to do the accounting on behalf of the franchisees in return for the respective fees.

2. Food processing, distribution and retailing revenues:

During 2019 and 2020, food processing and distribution revenue accounted for 21% and 17% of consolidated revenue, respectively.

2.1. The Company derives revenue from the production of a variety of food products: Revenues from food processing are recognised when the goods have been delivered to the end users.

2.2. Revenues from distributions: The Company earns revenue from the distribution of food and restaurant supplies to its Valentine and Casa Grecque locations. Revenue is recognised once the goods have been delivered to the franchise location.

2.3. Retail revenues: The Company earns revenues from the sale of products in retail shops. Retail revenue is recognised when the goods have been delivered.

3. Revenues from corporate-owned locations:

MTY not only operates with franchisees, but in some cases the restaurants are owned and managed by the same group.

Revenues from corporate-owned locations are recorded when services are rendered. Revenues from corporate-owned locations have accounted for 16% and 13% of total revenues in 2019 and 2020, respectively.

4. Promotional fund revenue:

Promotional fund contributions are based on a percentage of gross sales as reported by franchisees. Occasionally, the company charges a fee for the administration of promotional funds. Depending on the franchise agreements, franchisees are required to pay a fee ranging from 1% to 4% of gross sales, depending on the concept, to the promotional fund.

Promotional fund revenues have accounted for 16% and 17% of total revenues for 2019 and 2020 respectively.

2.3. M&A

MTY has a strong track record of deploying capital to execute cash flow enhancing M&A transactions. Many of the brands MTY acquires need significant work from an integration and process optimisation standpoint, which is where management has a long track record of successful transactions and ultimately reaping recurring cash flows from entitlements.

Acquisitions are the main growth strategy that the company will continue to pursue in the future, so this section explains the latest transactions and the multiples that the company has paid, and estimates the return that the company gets from these operations.

In the following image we can see the more than 50 acquisitions the company has made, where we will focus on the latest large M&A deals such as Kahala Brands Ltd in 2016, Imvescor Restaurant Group in 2018, Papa Murphy's in 2019 and the most recent acquisition Kuto Comptoir de Tartares in 2021.

Kahala Brands Ltd: On 26 July 2016, MTY announced that it had completed the acquisition of Kahala Brands Ltd for a purchase price of USD 394.2 million, executed with the issuance of 2,253,930 MTY shares and the payment of USD 212 million in cash. At closing, Kahala franchised and operated approximately 2,879 shops worldwide with 18 brands in 27 countries and generated approximately $950 million in system sales.

The objective of the transaction was to consolidate MTY's presence in the United States, as it would become an important growth platform for MTY's existing brands.

The shops acquired in the Kahala Brands Ltd. transaction have generated positive growth in MTY, driven primarily by the strong performance of Cold Stone Creamery (one of the 5 brands integrated with this acquisition), which accounts for about 10% of MTY's system sales.

The company paid pre-synergy EV/EBITDA multiples of 12.5x and post-synergy EV/EBITDA multiples of approximately 11.5x.

Imvescor Restaurant Group: On 1 March 2018, MTY, through the merger of a wholly-owned subsidiary with Imvescor Restaurant Group Inc. ("IRG"), acquired all of the outstanding shares of IRG. The total consideration for the transaction was USD 250.8 million, of which USD 53.1 million was settled in cash and the remainder in shares.

At the closing of the transaction, IRG operated 5 brands in Canada and had 261 locations in operation, generating an EBITDA of USD 18.5 million. The brands integrated into the group were: Baton Rouge, Score's, Toujours Mike's, Pizza Delight and finally Ben & Florentine. In this acquisition MTY paid EV/EBITDA multiples of 13x before synergies and 10x including synergies.

Papa Murphy's: MTY's last major acquisition, accounting for about 30% of sales. Conducted on 23 May 2019, the Company, through the merger of a wholly-owned US subsidiary with Papa Murphy's Holding Inc. ("PM"), acquired all outstanding shares. The total consideration for the transaction was $255.2 million.

Papa Murphy's operated 1,301 franchise shops and 103 corporate-owned shops in the US, Canada and the United Arab Emirates. It generated $28.8 million in EBITDA and the deal closed at 8.5 times EV/EBITDA.

It is interesting to explain the concept of Papa Murphy's, as it can be considered unique. The company focuses on selling raw pizzas for consumers to bake at home, orders can be placed in-store or online and all the products the company uses are very fresh, which is demonstrated by the fact that they do not use refrigerators.

On the negative side, this business model also competes with supermarkets, although the quality of the pizza is the differentiating factor of this business model.

Kuto Comptoir a Tartares: In terms of acquisitions, this is the most recent acquisition by MTY. It was announced on 1 December 2021, where MTY acquired Kuto Comptoir from Tartares, a high-growth company based in Quebec.

The other acquisitions MTY has made in recent years have paid multiples between 6x and 8x EV/EBITDA and 0.42x system sales, on average. The ROIC generated by these transactions can be estimated as follows:

If we consider the total investment in acquisitions that the company has made in a given period and how much they have contributed in cash flow, we can conclude that since 2009 acquisitions have had an average cash flow conversion of 12.61%.

Finally, acquisitions have contributed to an upward trend in the number of the company's outlets despite the fact that, as mentioned above, there has been a trend of net closures in recent years as a result of the change in business model.

We should not forget that 2020 was deeply affected by the pandemic, which led to major closures across the restaurant sector. However, this crisis may provide opportunities for MTY in the medium term to acquire companies at reasonable multiples, as it already demonstrated after the 2008 financial crisis.

3. EVOLUTION OF REVENUES

In this section we will look at the evolution of MTY's revenues and the factors that have been decisive in achieving its current growth.

Firstly, we must bear in mind that we are dealing with a high quality company that is very resistant to crises, as demonstrated by its revenue evolution between 2006 and 2010, where, despite the global financial crisis, it was able to triple its revenue, increasing its sales from 22 million to 66.89 million.

This growth was generated mainly thanks to M&A operations where the company was able to take advantage of the financial weakness of many companies to acquire them.

However, not everything is positive in the evolution of the company's sales, as the company's historical organic growth is slightly negative over the last 10 years (-1%, -0.5%). Despite this, starting in 2018 with the appointment of Eric Lefebvre as CEO, MTY aims to focus much more on the organic side of the business. This factor was not the main priority in the past.

Then, having understood that the company owes its growth to M&A operations, we can analyse that in the last 10 years the company has increased its sales with a CAGR of 23.1%, as shown in the following table:

In addition, the system's sales increased in the same period from 527 million to over 3500 million Canadian dollars, as shown in the graph below:

If we relate the sales of the system to the number of locations today, it can be concluded that the average revenue per restaurant has increased from $250,000 in 2011 to over $500,000 today. In the same period, the company spent approximately 1.2 billion on acquisitions, multiplying the number of locations by more than 3 times.

The geographic distribution of sales can be seen in the table below:

Despite the rapid growth in the United States resulting from the integration of Papa Murphy's Pizza and Cold Stone Creamery, the company's current market share in North America is still less than 1% of the market.

3. EVOLUTION OF EBITDA MARGIN

MTY's EBITDA margin is currently around 28%, as can be seen in the table below:

Although, it appears at first glance that margins have been declining since 2013, this is not entirely true. To understand this, we must bear in mind that MTY has several business segments, each with its own EBITDA margins. The following graph shows the weight of each business segment in the company's total revenues.

The food distribution and processing segment, which has lower margins, has considerably increased its weight in the company's overall revenues. As a result, overall margins decrease on paper and the company appears to be of lower quality, but in this case the opposite is true.

Franchise margins have not contracted; on the contrary, they are at their highest level in 10 years.

4. SHARE PRICE EVOLUTION

The evolution of MTY's share price has been incredible since its IPO in the 90s. It has managed to become a 100 bagger company, due to its excellent track record of generating recurring income through royalties and with a brilliant M&A strategy, where the management team has generated a lot of value for all shareholders.

5. SHAREHOLDERS AND MANAGEMENT TEAM

Stanley Ma, Chairman and Director: Stanley Ma founded the company and stepped down as CEO in November 2018. He is currently chairman of MTY. Although he is still active in pursuing, developing and negotiating mergers and acquisitions, he is no longer involved in day-to-day operations. Stanley is the company's largest shareholder, owning 16.2% of the shares, equivalent to 4,005,643 shares.

Eric Lefebvre, CEO and Director: Eric has been with MTY since 2009. He started as Vice President Finance, then became Chief Financial Officer between June 2012 and November 2018, and has since served as Chief Executive Officer of the Company. Prior to joining MTY, Mr. Lefebvre held leadership positions at Bell Aliant and Gaz Metro. He is a chartered professional accountant and holds an MBA.

Notably, when Eric was appointed CEO of the company, he was granted a package of stock options to keep him aligned with the company's objectives and growth. So now he not only owns 9,137 shares, but also a package of options on 240,000 shares.

Ren e St-Onge, CFO: She joined MTY in 2012 and replaced Mr Lefebvre as CFO of the company in November 2018. Like Eric, she holds a package of options on 40,000 shares. This aligns his interests with those of the shareholders.

On the other hand, based on the salaries and compensation received by key executives, it is noted that there is target-based remuneration.

For 2021, short-term cash incentives are based on achieving certain levels of organic growth in EBITDA, business units or brands, EBITDA targets and organic free cash flow growth, as well as new shop openings.

In terms of salary levels, Eric has the highest gross base salary of C$500,000, the other executives are in the range of C$250,000 to C$300,000.

If we compare what the managers finally earn, we can conclude that there is a greater interest in the evolution of the company going well, since around 20% of the shares in circulation are among the managers.

On the other hand, there are institutions with a large number of shares, such as Fidelity Management & Research and Company LLC and Fidelity Investments Canada, which own 13.29% and 10.29% of the shares respectively.

6. MARKET ANALYSIS

The fast food and restaurant industry is growing at over 3% per annum and is expected to continue to do so in the coming years.

We can also see that the US market, where the company has less than 1% market share, is 10 times larger than the market in Canada, which provides the company with many opportunities to increase its market share.

The following graph shows the main contribution to this growth reflected in the percentage of US and Canadian spending in restaurants:

On the other hand, with respect to COVID 19, the entire sector has suffered large drops in sales due to the mandatory closures, with some studies claiming that 20-25% of restaurants in North America went out of business due to the pandemic.

This reduction in restaurant supply is being felt in the sales and profits of restaurant companies, such as MTY, which, with fewer restaurants than in 2019, is generating higher profits.

In terms of restrictions during the pandemic, the United States has taken much less restrictive measures than Canada, which has been noticeable in the evolution of sales during the year. Restrictions in Canada can be expected to ease in the course of the coming quarters, where there is an even higher percentage of closed restaurants.

However, it can be concluded that the market environment remains difficult, with much uncertainty about new strains of coronavirus that may cause further mandatory closures. Nevertheless, the restaurants that adapt best may benefit and may even take advantage of the moment to make M&A deals.

7. COMPETITIVE ADVANTAGES

Brand diversity: The great diversity of concepts allows MTY to position itself in a wide range of sectors and segments of the population, in addition to having the possibility to gather information to install new concepts in existing locations.

Cost structure: Unlike a restaurant that has very high fixed costs such as the rental of the premises or the number of permanent staff, MTY does not have to rent these premises, since, as explained above, they are sublet to the franchisee. The variable cost of food in case of inflation can benefit the company because they charge a royalty on the income but without assuming the increase in the cost of food.

Management team: The management team has proven to be of great value to all shareholders, managing to scale the business through M&A transactions with a successful track record.

Crisis resilient business model: In 2008 and 2009, during the financial crisis, the company's comparable sales fell by only 1.9% while total sales increased by 55%, which was generated by the opportunity to acquire companies at very good prices.

8. RISKS

Negative comparable sales: As explained throughout the investment thesis, MTY has negative comparable sales in recent years, however this has not prevented the share price from increasing several fold due to its strength in generating inorganic growth through M&A transactions. However, I consider it a risk that buyable sales could reach a level of more than -3%.

Net site closures: Excluding the restaurant acquisitions the company has made, franchisees have had net closures over the past few years, which means that not all franchisees are succeeding in their restaurants. Although it should be noted that the franchises that have closed are less profitable than the new ones that are opening.

Covid 19: New strains of coronavirus may cause further mandatory restaurant closures as was the case in 2020, this situation may further deteriorate the sector and cause many MTY franchisees to go out of business.

M&A risk: MTY, as explained above, focuses its growth on carrying out M&A operations, so despite having a management team with a great track record, with more than 50 successful acquisitions, there is always a risk linked to this type of operation.

9. BUSINESS PLAN

In this section, I will establish my estimates for the period 2022-2026 in order to project the company's financial statements and obtain the intrinsic value of the company, by means of valuation by comparable multiples.

9.1. Estimates 2022 - 2026

I will set the valuation assumptions in two scenarios, the first one I will call the "normal scenario", to which I assigned a higher probability of occurrence, and secondly, an "unfavourable scenario" in which the company's growth will be tested.

Before I start with the scenarios, I would like to explain several details that MTY has, which are important to know in order to be able to make a correct assessment.

The CAPEX of the company is practically zero or negative, this is because, when a franchisee stops paying or closes its restaurant, MTY keeps the restaurant for free, being able to sell to another franchisee and benefit from the transfer of the premises at zero cost or as a second option it can sell its assets and reach an agreement with the main lessor, as MTY has made many improvements to the premises.

In the following image extracted from the 2020 annual report, this case of zero or negative CAPEX can be seen:

We note, that in both years (2020 and 2019) the item "Proceeds on disposal of property, plant and equipment, assets held for sale and intangible assets" is higher than the additions in plant and equipment and intangible assets. This is due to the explanation I have given above.

On the other hand, it is necessary to take into account the company's acquisition policy and the cash flow conversion of these transactions, as discussed in section "2.3 Company's M&A strategies".

Normal Scenario:

In the following, I will mention the key factors of this scenario:

Revenues: MTY is a company that has grown sales at a CAGR of 20% over the last 10 years, so in this normal scenario, I will project sales at 15% per year, taking into account that the COVID has left many companies impaired and MTY can take advantage of this to make acquisitions. As for organic growth, I see it at around 0%.

Debt: It should be noted that I have not taken into account the leases in the debt, as MTY subleases them to franchisees, and with regard to its projection, it will be linked to the company's M&A operations.

M&A: I have taken into consideration as I have mentioned above an inorganic growth of 15%, so the company will continue to deploy capital towards M&A operations, in which I will estimate that MTY will pay per acquisition, an average of 7x EV/EBITDA pre-synergies. In addition, the FCF that the company generates during the year to meet these acquisitions and the constraints that exist under the covenants have been taken into consideration.

CAPEX: As explained, CAPEX is very low, close to 0, so in this scenario I have considered an investment equivalent to 1% of sales.

Margins: In this scenario I consider an EBITDA margin in line with recent years at around 30%.

Unfavourable Scenario:

The key factors in this scenario are as follows:

Revenues: In this scenario, I will see a more difficult environment for the company, where organic growth averages -0.5% and inorganic growth is only 7-8%.

Debt: It should be noted that in the debt I have not taken into account the leases as MTY subleases them to franchisees and with respect to its projection, having a lower inorganic growth it will be able to allocate much of the FCF to pay debt, so it is expected in this scenario that the company will end 2026 with net cash.

M&A: I have taken into consideration as mentioned above an inorganic growth of 7-8%, so the company will continue to deploy capital towards M&A transactions, in which I will estimate that MTY will pay an average of 7x EV/EBITDA pre-synergies per acquisition.

CAPEX (unchanged from previous scenario): As explained the CAPEX is very low close to 0, so in this scenario I have considered an investment equivalent to 1% of sales.

Margins (unchanged from the previous scenario): In this scenario I consider an EBITDA margin in line with recent years at around 30%.

9.1. Projections 2022 - 2026

NORMAL SCENARIO

As can be seen in the projections of the profit and loss account, EBITDA has increased by 151 million, as a result of acquisitions, where if we establish an average of 7 times EBITDA for each one of them, we would arrive at an approximate investment of 1061 million in M&A operations.

Then, the FCF during the projection period has been 1009 million, increasing by 118 million from 2022 to 2026, where the historical profitability of the acquisitions was considered.

The following summary table shows the projection of the main financial parameters:

Debt can be estimated to be stable during this period, as the projected acquisitions are almost entirely covered by the FCF generated.

UNFAVOURABLE SCENARIO

In this scenario, the company has a slightly negative organic growth and as a result of acquisitions EBITDA increased by 50.3 million up to the period ending 2026. Considering the same EV/EBITDA multiple as in the previous scenario, we conclude that an investment of approximately 360 million is needed in M&A transactions.

However, contrary to the "normal" scenario, the FCF generated annually by MTY allows the company to make these acquisitions and allocate around 70 million annually to debt repayment.

The company will end up with net cash of 70 million in 2026.

9.2. Comparable Multiples

In this section, we will analyse the comparable companies to MTY, both in Canada and the United States, in order to estimate the average multiples at which these companies are listed.

* It is important to note that the study has been carried out considering the average of the multiples over the last 5 years (EV/EBITDA and P/FCF), since with the current market conditions and the large injections of liquidity that have taken place since 2020, many of the companies comparable to MTY have had an unprecedented expansion of their multiples.

In this study, we can see how MTY has always traded at a discount to comparables, in addition to the companies mentioned in the study, other companies in Canada can be added, although of smaller capitalisation, such as:

-

Pizza Pizza Royalty: which through its subsidiary, Pizza Pizza Royalty Limited Partnership, owns and franchises quick service restaurants under the Pizza Pizza and Pizza 73 brands in Canada. They also sell food and beverages. As of 31 December 2020, the company had 749 restaurants in the royalty group. Pizza Pizza Royalty Corp. was founded in 1967 and is headquartered in Toronto, Canada.

It trades on average at 13x EV/EBITDA and 18x P/FCF.

-

Boston Pizza Royalties Income Fund, operates as a franchisor of pizzerias and casual dining pasta restaurants. As of 1 January 2021, the company's franchise system consisted of 387 restaurants in Canada. Boston Pizza Royalties Income Fund was founded in 2002 and is based in Richmond, Canada.

It trades on average at 13x EV/EBITDA and 17x P/FCF.

Valuation

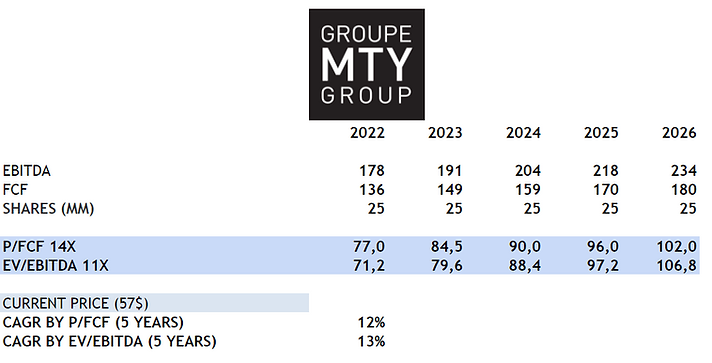

Normal Scenario:

After having analysed MTY's North American comparables, I have decided to value the company at 14x EV/EBITDA and 17x P/FCF, being its historical average.

Although the comparables trade at higher multiples, it is more sensible to use the multiples I have just mentioned, as these other companies have a larger market capitalisation and a larger analyst following.

Unfavourable scenario

In this scenario, due to lower growth of the company, I will apply multiples of 11x EV/EBITDA and 14x P/FCF.

10. CONCLUSION

After having analysed MTY in depth, I can conclude that we are dealing with a high quality company, with a business model with recurring income that is very resistant to crises. Furthermore, the management team is aligned with the interests of the shareholders and is made up of excellent professionals who have been able to successfully carry out more than 50 M&A operations.

The company operates in a very fragmented market so there is still plenty of room to allocate capital and create value, with respect to risk factors such as negative comparable sales, the entry of Eric as the new CEO, aims to focus on organic growth and not only inorganic as it had been doing until 2018.

Finally, the valuation by comparable multiples yields positive returns in both "normal" and "unfavourable" scenarios, with 5-year annualised returns in double digits.

*The MTY FOOD GROUP Investment Thesis was published on this website on 07/12/2021, and in case of needing an update due to company results publications or sector highlights, a direct link will be left at the end of this thesis.

Disclaimer

The publications on this website are not investment advice. All contents of this website and newsletter, and all other communications and correspondence from its author, are for informational and educational purposes only and in no way, whether expressed or implied, shall be considered investment advice, legal or otherwise. Do your own research and due diligence.